We have all become used to talking about the various “colours” of “low carbon hydrogen”. When we talk about “blue” or “green” hydrogen, we know we are referring to something whose production is meant to result in fewer greenhouse gas (GHG) emissions than producing standard “grey” hydrogen by reforming methane and venting the waste CO2. However, if, like the UK government, you are going to spend large amounts of public money subsidising the production of “low carbon hydrogen”, with a view to hitting net zero targets, you need to be a good deal clearer about exactly what you are getting.

In this post, we look at two documents: Consultation on a UK low carbon hydrogen standard (Consultation), and an accompanying consultants’ report on Options for a UK low carbon hydrogen standard (Options Report). They were published by the UK’s Department of Business, Energy and Industrial Strategy (BEIS) on 17 August 2021. For background, a full list of the BEIS hydrogen policy documents published on that date and a discussion on the UK’s overarching Strategy, click here.

This is not the first time the UK government has consulted on a low carbon hydrogen standard. It first did so (although only in relation to green hydrogen) in 2015. Since then, as the Options Report outlines, other hydrogen standards have started to occupy the field, including CertifHY, TÜV SÜD, and emerging Chinese and Australian schemes. The EU’s second Renewable Energy Directive’s provisions on “renewable fuels of non-biological origin” (which include those containing green hydrogen), and their implementation, have also forced consideration of a number of key issues. However, for the moment, as the Consultation points out, there is “no single understanding or formal definition of what is actually meant by ‘low carbon’ hydrogen in the UK”, and this gaps needs filling.

Spoiler alert

If you have ever thought about what a low carbon hydrogen standard might look like, you will have got as far as thinking in terms of a limit based on GHG emissions. You might have thought that such a limit could either be set very low – thus potentially including only “green” hydrogen produced by electrolysis using 100% renewable electricity, or somewhat higher – thus also including “blue” hydrogen produced by methane reformation with efficient CO2 capture and storage. But essentially, you were probably thinking in terms of a single, headline threshold figure.

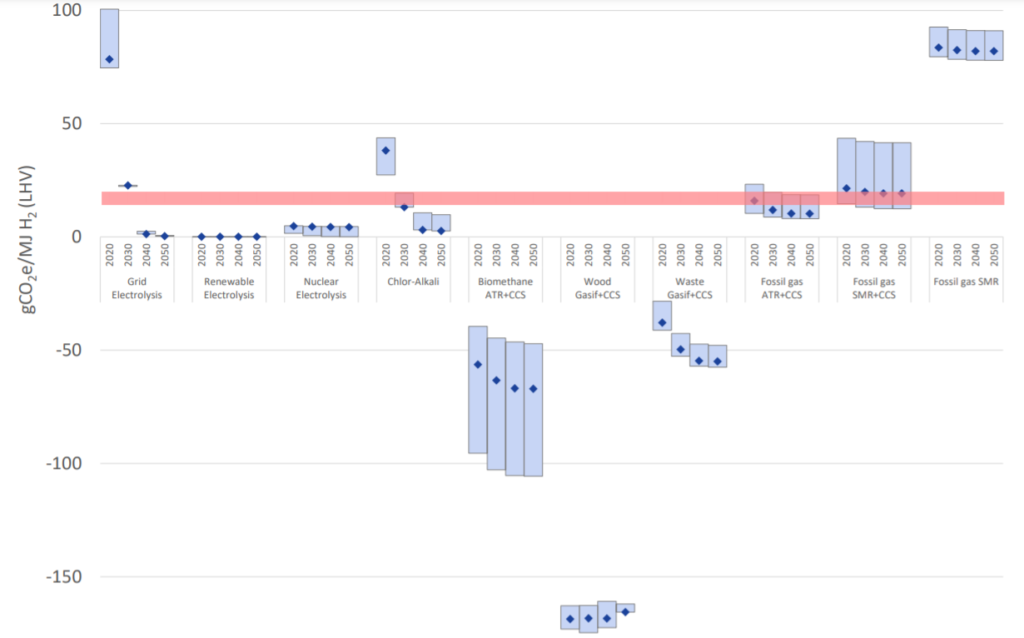

The Consultation does not suggest what the headline GHG emissions limit of a future UK low carbon hydrogen standard should be. However, it does include a graph – Figure 2, reproduced below – which usefully indicates how the consultants who produced the Options Report think that different production technologies compare in terms of emissions intensity. The blue bars in the chart are estimates of the range (from high to low) of GHG emissions associated with different hydrogen production techniques at different points in the next 30 years (with the blue diamonds representing the central estimate of emissions for each technology). The red line indicates “the potential impacts of an example threshold of around 15-20 gCO2e/MJLHV of produced hydrogen”. In other words, if a figure in that range were chosen as the standard, those technologies that are above the line would likely not meet the standard, and therefore not qualify for public financial support, while those technologies that are below the line would meet the standard and qualify for support.

Policy context

The Consultation makes it clear that BEIS wants the standard to encourage, not inhibit, new hydrogen production. Compliance with the standard would be one of the determinants of eligibility for financial support via the UK’s hydrogen “business model” or Net Zero Hydrogen Fund. The Consultation stresses that it is important to ensure that “any investment made today is directed towards production technologies that are consistent with the UK’s net-zero commitments and carbon budgets”.

The Consultation makes it clear that BEIS is engaged with other bodies that have set or are formulating similar standards in other countries and internationally. It is also alive to the possibility of both imports and exports of hydrogen to and from the UK. However, its focus is primarily on domestic production and consumption of low carbon hydrogen.

The aim is to establish a GHG emissions standard for low carbon hydrogen that meets the eight criteria of being inclusive (e.g. technology neutral); accessible (cost-effective, simple and user-friendly); transparent; compatible (working with other UK energy sector schemes and other countries’ standards); ambitious; accurate; robust (with strong penalties for fraud etc.); and predictable.

Multiple variables

The Consultation outlines the many points that need to be decided when establishing a standard, in addition to the headline emissions figure. These include:

- Matters of scope: Should the standard cover only hydrogen produced and used in the UK? Should it reflect emissions only up to the “point of production” (BEIS’s preference) or some downstream emissions too? Should “production” emissions include those that are “embodied” in equipment or associated with the production of natural gas?

- Accounting for electricity emissions: BEIS seems wary of adopting a standard that would limit support only to projects with off-grid renewable generation dedicated entirely to hydrogen production. However, should the standard go as far as allowing production by any grid-sourced electricity (see the graph above)? If it is limited to production from renewable power only, should that be on the basis of claims based on production from grid-connected renewables physically linked to the electrolyser, or also on trading and the cancellation of guarantees of origin? Should other conditions be imposed (e.g. temporal or geographic constraints designed to ensure the electrolysers support rather than undermine grid stability)? Perhaps most important is the vexed question of “additionality”: should the standard cover only hydrogen produced from new renewable electricity generating capacity built for that purpose, rather than encouraging its production from other existing or future renewable generating capacity, thereby delaying decarbonisation of the grid – and, if so, how?

- Other accounting matters: Should there be physical traceability of emissions, through a mass balance system, or should a “book and claim” (certificate trading) system be followed? Should carbon captured and used – rather than stored – in blue hydrogen production count as GHG emissions avoided for this purpose, and if so under what conditions? How do you prove that captured CO2 will not return to the atmosphere over an agreed minimum period of time in this context? How do you account for waste fossil feedstocks or mixed inputs (e.g. if a plant uses a mixture of “clean” and “dirty” electricity sources to power its electrolyser, do you average their emissions over its whole output, or divide its output into green and grey batches)?

- Core measurement issues: Do you measure how many kgCO2e are emitted per kg of hydrogen produced, or how many kgCO2e are emitted per MJ Lower Heating Value or per kWh Higher Heating Value? BEIS prefers the latter. How do you deal with negative emissions (see the chart above) or measure any non-GHG impacts that may be taken into account (e.g. water consumption or air quality)? Finally, should the GHG threshold itself be defined in absolute terms or in relative terms (e.g. by reference to a fossil fuel comparator)?

- One size fits all? Whilst BEIS is clear that it wants a standard that applies across technologies, it leaves open the possibility of there being more than one threshold. There could be more less demanding thresholds, as in some existing schemes. As the market evolves, the Consultation also suggests that thresholds may tighten over time, but without retrospectively depriving projects that met an earlier applicable threshold for support.

- Administrative details: Who is going to run the standard? Will it work on “default” or “actual” emissions data? Who will report (and verify/audit) each participant’s emissions?

All told, respondents are asked no fewer than 42 questions (many of which have more than one part). In many cases, the Consultation does not indicate BEIS’s preferred position, although the Options Report (chapter 6) does include traffic-light coded tables that evaluate each set of options against the eight criteria mentioned above, and the consultants make recommendations based on these.

What next?

BEIS expects “to finalise design elements of a UK low carbon hydrogen standard by early 2022”. In early 2023, it aims to be signing the first contracts under the hydrogen business model, and those involved will need a clear understanding of the standards they will be committing to by then, if not sooner. There is clearly a lot of detailed work to do in a relatively short space of time.

As the Consultation and Options Report show, there are a number of trade-offs to be made in reaching a view on the many choices inherent in specifying a low carbon hydrogen standard. Strategically, perhaps the dominant one is between a “higher” standard/higher initial subsidy costs/lower initial production volumes and a “lower” standard/lower subsidy costs/higher initial production. Arguably, though, the true test of a low carbon hydrogen standard will be how it is received in the market. For example, if today you set up “gold” and “silver” standards, and subsidise projects that meet either, what happens if, when the subsidy contract ends in 2035, the market for low carbon hydrogen that you have succeeded in stimulating has no interest in “silver”-compliant hydrogen?

It is not obvious that there are “right answers” to many of the questions in the consultation, in the overall context of developing a UK hydrogen sector. As usual, the policy will only be as good as the inputs to it. If you have views on the questions raised, you have until 25 October 2021 to respond. We would be happy to help you put your case to BEIS.